Unaffordable Housing: Why Housing is So Expensive and What We Can do About It

America has a housing problem that keeps getting worse. Too many Americans can’t afford a decent place to live.

Demographic and economic trends have combined with bad policy to make both renting and buying increasingly unaffordable in large parts of the country, and that was before the COVID-19 pandemic pushed the U.S. unemployment rate to levels last seen during the Great Depression.

As policymakers work to address the near-term crises of potential evictions, mortgage defaults, and foreclosures, this New Center paper explores the longer-term causes underpinning housing affordability and common-sense solutions to fix it.

Over the past few decades, American cities have become more desirable places to live. They are safer and more convenient than they were in the past, and, pre-COVID, their residents enjoyed an abundance of job opportunities and amenities. Certain generational trends also increased demand for urban living. On average, millennials are waiting longer than previous generations to marry and start families. Single-person households have increased by 22% since 2000.

Compared to previous generations, baby boomers are living longer and are more likely to be divorced and living alone. As a result, many single baby boomers have downsized and moved into entry-level homes and apartments in cities and surrounding areas, providing a new source of housing competition to younger adults.

In the early 2010s, urban population growth outpaced suburban growth for the first time since the 1920s. But in the years since, the supply of affordable housing in cities has not kept pace with surging demand, which has led prices to skyrocket and forced people who might have otherwise preferred city life to once again head for the less-expensive suburbs.

Since the onset of the COVID-19 pandemic and social unrest in U.S. cities, there’s been anecdotal reporting and early data to suggest the urbanization trend is reversing as people seek homes in the suburbs.

It’s too early to know whether this represents a temporary trend or a durable change in housing preferences. But when the COVID-19 pandemic ends and America is able to return to some semblance of normal, policymakers and the public will still be faced with the same fundamental problem: too many Americans can’t afford a decent place to live.

The Problem

Widespread housing unaffordability is a problem that’s hard to solve but easy to explain. There simply aren’t enough homes being built to keep up with the number of people who need them.

The shortage of all types of housing has increased costs to the extent that many working and middle-class people cannot afford to rent or buy a place to live. According to a March 2019 Cato Institute/YouGov poll, 56% of Americans reported that expensive housing costs had prevented them from moving to a better neighborhood. In the same poll, 61% reported making at least one sacrifice in the past three years because they were struggling to pay for housing.

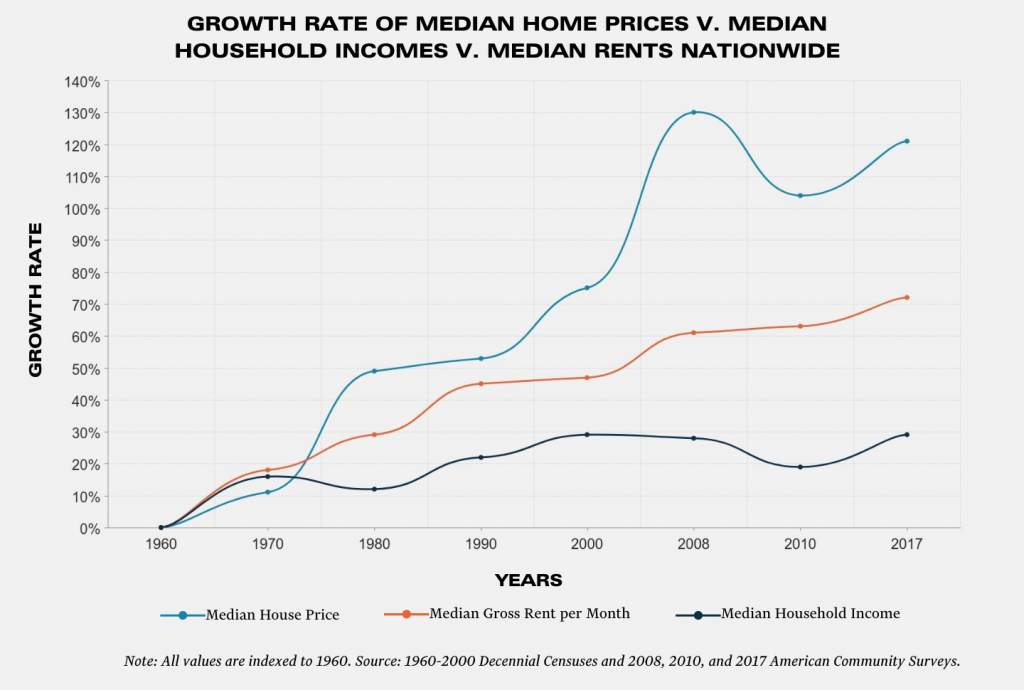

The Harvard Joint Center for Housing Studies estimated in 2019 that 37.8 million renter and homeowner households were “cost burdened,” a term used to describe those who spend at least 30% of their income on housing. Housing supply has lagged behind growing demand, and housing prices have well outpaced wage growth (see chart below). The problem will become worse each year if supply does not drastically increase: Freddie Mac estimates demand for housing at about 1.62 million units per year, and the current annual rate of supply falls about 370,000 units short of that.

The lack of affordable housing is harming both renters and buyers. Prospective first-time home buyers are directly impacted by rising prices in both markets: the more a household spends on rent, the less they have left over at the end of the month to save for a down payment on a home purchase.

More recently, the economic crisis sparked by COVID-19 resulted in mass layoffs, leaving millions of Americans without sufficient income to cover rent and mortgage payments. The COVID-19 Eviction Defense Project estimates that about 20% of all renter households are at risk of being evicted by September 30, 2020, and according to a survey conducted by Apartment List, 30% of homeowners could not afford their full mortgage payments in July. According to an annual Gallup survey, 39% of Americans were at least somewhat worried about being unable to pay rent, mortgage, or other housing costs in April of 2020—a 9 percentage point increase from last year’s survey.

The CARES Act, passed in March 2020 in response to COVID-19, offered expanded unemployment benefits and $1,200 Economic Impact Payments (stimulus checks) to help families stay afloat, but they have not been a panacea. A May 2020 poll conducted by Hart Research Associates on behalf of the nonprofit Opportunity Starts at Home found that, among those who applied for unemployment benefits as a result of COVID-19, 31% do not believe these benefits will be sufficient to cover their basic living expenses, including housing costs, over the next several months. The unemployment insurance expansion included an additional $600 per week for each recipient on top of regular state unemployment benefits, but this provision expired at the end of July.

The Rental Market

According to Harvard’s Joint Center for Housing Studies, 47.5% of renters were paying more than 30% of their income to cover housing costs prior to COVID-19—a near doubling of the 23.8% observed in the 1960s.

In 95% of U.S. counties, a full-time worker earning federal or state minimum wage cannot afford to rent a modest, one-bedroom apartment. Rental prices in the U.S. are out of reach even for many middle-class renters earning more than the national average renter’s hourly wage of $18.22. The hourly wage required to afford renting an average apartment is $19.56 for a one-bedroom and $23.96 for a two-bedroom.

As a result of the current economic crisis sparked by COVID-19, many Americans who have lost income are looking for cheaper rental housing. Many others who can afford to stay put are choosing to wait out the pandemic in place even if they previously had other plans. The result has been less rental turnover than what is typically expected.

A recent Washington Post story interviewed local real estate agent Hugo Romero, who explained, “The reduction in the inventory, I believe, is also directly related to the pandemic, as people put their plans on hold whether voluntarily or involuntarily. Tenants did not move out as expected, and also homeowners that were going to move away for jobs, especially with the military and federal government, and would have rented their properties, ended up not moving.”

In the wake of the pandemic, rent price growth has slowed nationwide, but this is largely the result of demand shifting from mid-range and luxury rentals to more affordable units. It is not yet clear how the market might rebound, but rental prices are still out of reach for the most economically vulnerable Americans.

The Buying Market

For the past century, buying a house has been synonymous with achieving the American Dream. But homeownership is becoming increasingly unrealistic for many Americans. In 1960, the average household could expect to spend 2.1 times their annual income on the purchase of a home. By 2017, it had risen to 3.6 times the average household income.

A study of housing price data from Q2 of 2020 found that the median home price was unaffordable for the median wage earner in 74% of U.S. counties. Between June 2019 and June 2020, the national housing declined by 27.4%. This trend helps explain why the nationwide renter population has increased by 9.1% since 2010—more than double the 4.3% growth of the homeowner population.

COVID-19 and the resulting economic crisis have resulted in mortgage interest rates reaching record lows, and these low rates have led to a surge of new mortgage applications and demand for homes. At the same time, supply has remained low. This has prevented the price drops home buyers might typically benefit from in a recession.

“Housing affordability is a little easier on paper with low mortgage rates, but the bigger challenge is trying to find a home,” Realtor.com director of economic research Javier Vivas told USA Today. “Housing demand has increased beyond expectations. When you combine that with historically low levels of inventory, it’s a perfect storm for increased competition and an affordability crisis.”

As Mike Fratantoni, chief economist of the Mortgage Bankers Association, explains to the Washington Post: “We’re going to have this really surprising situation where, even though demand has certainly been impacted by the much weaker job market, supply has fallen even more. Prices, as a result, are going up at the time that we’re in, in this very deep crisis.”

Broader Economic Consequences

Cities that contribute the most to American economic growth could be contributing even more if not for the affordable housing shortage, and this untapped potential is largely due to “spatial mismatch”—a discrepancy between where jobs are located and where potential employees live. Prohibitive housing prices not only prevent potential workers from moving to the cities or neighborhoods where they could be the most productive, but they also impede overall economic growth in these areas.

In theory, productive cities with the best opportunities for economic mobility should attract waves of new workers and the construction of new housing to accommodate them. As a city’s productivity grows, wages should grow as well. But unaffordable housing prices serve as a major obstacle for potential workers who wish to relocate. Many are left with no choice but to forego desirable job opportunities. As a result of this spatial mismatch, workers, businesses looking to hire, and the economy at large all suffer.

A study from the Urban Institute shows that spatial mismatch is pervasive in American cities, particularly with respect to lower-income households and hourly wage jobs. Using data from Snag, an online job board for hourly wage jobs, researchers found that job postings in the San Francisco Bay Area and Columbus, Ohio outnumbered potential job seekers living within a reasonable commuting distance of those jobs. Several economic studies have examined the effects of increased population density on economic output. While the predicted effect size ranges from about 6% to 28% across studies, the general consensus is that doubling urban density would raise a city’s economic productivity significantly.

Of course, doubling the density of a city like New York—the U.S. metropolitan area with the highest population-weighted density—might not be possible or desirable in the new pandemic era. And if it was, it certainly would not be without negative consequences including stresses on local infrastructure and transportation networks. But other highly productive U.S. cities do have the space for at least some increase in density. Los Angeles, the next-densest metro area, is less than half as dense as New York in terms of people per square mile.

In the time of COVID-19, the concept of increased housing density has come under scrutiny, as many have assumed that density is the culprit in the spread of the virus. New York Governor Andrew Cuomo has even perpetuated the idea, remarking in a COVID-19 press conference that “it’s about density… Dense environments are [the virus’s] feeding grounds.” But a June 2020 study conducted by Shima Hamidi of the Johns Hopkins Bloomberg School of Public Health found no relationship between county density and incidence of COVID-19 infections. In fact, higher density was associated with lower death rates, presumably because of easy access to quality health care in population-dense places. How, then, can we explain the catastrophic outbreak that occurred in New York City? Connectivity, rather than density, appears to be the driving force behind the spread of COVID-19.

Similarly, Will Imbrie-Moore of the Harvard Political Review writes, “Coronavirus is transmitted not through the walls of urban dwellers’ neighboring apartments but within the business establishments, hospitals, and other public places that all essential workers—urban, suburban, and rural—must frequent daily.”

In the post COVID-era, the rise of remote work and the ability of workers to live in entirely different regions than their employers could certainly ease some of the housing affordability and availability issues in major urban centers.

Even so, many areas will still require significant increases in housing supply to better match local demand. It’s an obvious solution to this pressing issue. So why hasn’t it been done?

Across the country and at all levels of government, outdated and ineffective housing policy has created significant obstacles that stand in the way of meaningful progress. To overcome these obstacles and pave the way for effective change in both the short term and long term, The New Center offers the following suggestions:

To local governments:

- Emulate other localities that have enacted promising zoning reforms such as

- Allowing for more residential development options in areas currently zoned exclusively for single-family construction

- Reducing minimum parking requirements associated with multifamily development to free up residential land and decrease unnecessary costs

- Relaxing regulations that explicitly limit density

To the federal government:

- Provide direct aid to landlords and mortgage lenders who have lost income as a result of the pandemic

- Require localities to meet certain supply-side policy standards to become eligible for federal transportation funding

- Enact bipartisan legislation to prevent Housing Choice Voucher discrimination

Barriers to Building More Housing

- Archaic zoning and land use regulations impede the construction of new housing supply

In the introduction of the 2018 book Parking and the City, UCLA urban economist Donald Shoup writes:

“At the dawn of the automobile age, suppose Henry Ford and John D. Rockefeller had asked how city planners could increase the demand for cars and gasoline. Consider three options. First, divide the city into separate zones (housing here, jobs there, shopping somewhere else) to create travel between the zones. Second, limit density to spread everything apart and further increase travel. Third, require ample off-street parking everywhere so cars will be the easiest and cheapest way to travel.”

Many of the zoning and land use regulations in today’s American cities and towns are relics of a time when car travel was the predominant means of transportation. Today, large cities rely on alternatives such as public transportation and bike lanes to alleviate car traffic and accommodate growing populations. Despite these changes in transportation, local housing policy has failed to adapt. Three types of regulation—parking requirements for new residential construction, single-family zoning, and density regulations—are especially harmful to housing production and affordability. These policies also perpetuate the racial and socioeconomic segregation still prevalent across the country.

Although driving is no longer the only option for transportation, most local governments still require developers of multifamily housing to provide a minimum number of off-street parking spaces to accompany a new building—regardless of whether or not residents plan to use them. As a result of parking minimums, off-street parking spaces in the U.S. outnumber DMV-registered cars by a ratio of 3:1. These laws exacerbate the affordable housing shortage by inhibiting supply and increasing costs. Parking spaces occupy land that would have otherwise been available for residential development, and parking construction significantly increases construction costs. This burden is transferred to renters and buyers in the form of higher housing prices.

These extra costs are regressive—lower-income households are less likely to own cars and therefore less likely to receive any benefit in exchange for their extra payment. According to the Victoria Transport Policy Institute, the requirement to supply one parking space per unit in a typical affordable housing development increases development costs by 12.5%—a deterrent to potential developers and an increased cost burden on renters. Some cities have recently enacted reforms to relax parking requirements, and others like San Francisco, Buffalo, and Minneapolis have completely eliminated them.

In order to preserve the suburban way of life that widespread car ownership enabled in the post-World War II era, municipalities also began to impose regulations to limit population density on residential land. These regulations can still be observed almost everywhere in the U.S., and they raise housing prices by limiting supply. According to a study by Gallup Principal Economist Jonathan Rothwell, anti-density regulations alone account for about 20% of the variation in metropolitan housing growth.

A minimum lot size requirement is one such density restriction that specifies the square footage each plot of residential land must meet or exceed. Under these requirements, people and developers purchase more land than they otherwise would, leaving less land available for development. A study of minimum lot size requirements in Massachusetts conducted by Harvard economist Edward Glaeser found that each additional acre required per lot was associated with a 40% decline in new construction permits granted between 1980 and 2002.

Residential developers in most cities do not have free reign to build any type of housing anywhere they would like. Usually with some valid reason, state and municipal governments do not permit residential development on dangerous terrain (flood plains, for example), protected wildlife habitats, or land set aside for other types of development. But less justifiable are many of the zoning regulations that permit some types of residential development but not others.

Across the U.S., residential land use policy heavily favors detached single-family housing—the least efficient type of housing in terms of energy and land usage, cost, and number of people accommodated—at the expense of multifamily housing (apartment or townhome complexes, for example). 75% of all residential land in many U.S. cities is zoned exclusively for single-family development, and this percentage is even higher in suburban areas. As cities and suburbs grow, limitations on multifamily development only contribute to the problem of inadequate housing supply.

Several studies connect strict zoning and land use laws to housing supply reductions, higher housing prices, and unfavorable economic outcomes in general. An analysis of Massachusetts rental housing data by Brookings urban economist Jenny Schuetz found that zoning and land use restrictions do limit construction of multifamily housing. Between 2000 and 2005, municipalities with stricter zoning laws issued significantly fewer multifamily building permits than those with fewer restrictions. Strict residential land use and zoning laws effectively thwart economic mobility by preventing low and middle-income individuals from relocating to the places where the best jobs are located.

A 2015 report from the University of Chicago Law School offered an astounding estimate: if the strict land use regulations in New York, San Francisco, and San Jose were only as stringent as those of the average American metro area, the overall size of the U.S. economy would be 9.5% larger. This number accounts for the increased wages workers could earn if they were able to afford housing in these cities and productivity gains for companies if housing costs did not prevent them from attracting enough workers.

Despite the widespread negative effects of strict residential zoning regulations, these laws are still pervasive in cities across the country. A major explanation as to why these types of laws stay in place is that current residents advocate for their preservation. Ryan Avent, senior editor at The Economist and author of The Gated City, explains:

“The residents of America’s productive cities fear change in their neighborhoods and fight growth. In doing so, they make their cities more expensive and less accessible to people with middle incomes. Those middle-income workers move elsewhere, reducing their own earning power and the economy’s potential in the process.”

Some local governments have recognized the harms of strict residential zoning policies and introduced proposals to change them. A core tenet of many of these proposals is “upzoning,” which involves the amendment of laws that limit residential development to single-family detached housing to allow for the construction of multifamily housing as well. But many of these proposals have failed to pass. Those already living in an area—often wealthy residents—fear that new development and new neighborhood residents will bring unwanted change in the form of extra traffic, overcrowding, and noise, and they vocalize these beliefs at city council meetings and at the voting booth.

Analysis of municipal data by political scientists at Stanford found that socioeconomic status was a strong predictor of political engagement. Homeowners living in the most expensive homes were significantly more likely than other groups to vote in local elections, especially when land use regulations were in question.

To make matters even more difficult for legislators hoping to pass reforms, tenant activists in some places have become unlikely allies to wealthier residents in opposing new development. Many believe that upzoning would exclusively result in the construction of new luxury apartments and condos, increase rent prices, and displace low- and middle-income residents.

Evidence suggests the opposite: cities with the most restrictive land use policies are the ones that see the most luxury development as a proportion of all new construction. Any type of new supply—even a luxury apartment complex—absorbs some demand and works to slow price increases in the surrounding area.

NYU urban economist Xiaodi Li found that the construction of new high rise buildings in New York does lead to new amenities in the surrounding area that may slightly increase rent prices. But the effect of new supply more than makes up for it. Overall, the study finds that every 10% increase in housing supply lowers rent and sales prices by 1% for high-end and midrange properties within 500 feet of new supply. It should be noted that new luxury construction in this study neither increased nor decreased the cost of lower-income housing nearby—the two markets do not directly compete with one another.

- Federal housing subsidies and tax benefits have notable shortcomings

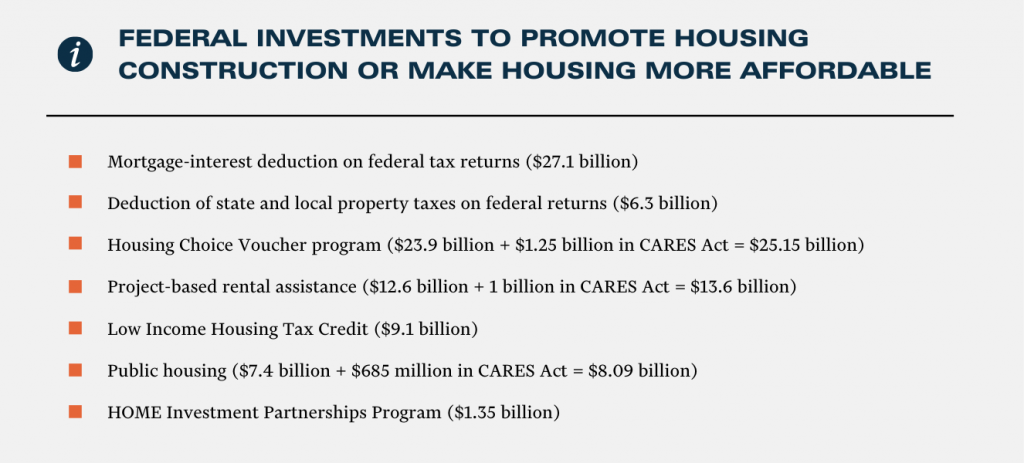

The U.S. Department of Housing and Urban Development (HUD) has several programs in place to encourage the construction of affordable housing and ease cost burdens for those who qualify. And the federal tax code offers several benefits aimed to encourage homeownership by making it more affordable. But despite these massive spending efforts and the infusion of extra funding for certain HUD programs outlined in the CARES Act, the government falls short of reaching its intended goals.

*Expenditures are 2020 projections based on Treasury Department reports, approved HUD budget, and additional allocations outlined in the CARES Act.

The mortgage-interest deduction (MID) aims to ease the burden of purchasing a home by allowing homeowners to deduct the interest paid on their first $750,000 of mortgage debt when filing federal taxes. But a large portion of the benefits do not accrue to the homeowners who need them the most. In 2018, 80% of MID benefits went to households in the top 20% of the income distribution. It is commonly believed that the MID is effective in promoting homeownership, but evidence from other countries suggests this might not be the case. Canada, the United Kingdom, and Australia offer no similar subsidies, but homeownership rates in these countries are slightly higher than in the U.S.

Homeowners must pay property taxes to their state and local governments, but they may deduct them up to a limit of $10,000 when filing their federal income tax returns (known as the SALT deduction). However, the benefits of the SALT deduction are not evenly distributed to all homeowners. They disproportionately accrue to those on the higher end of the income spectrum, in part because it often makes the most sense for lower-income households to claim the standard deduction rather than itemizing. According to the Urban-Brookings Tax Policy Center, only about 21% of taxpayers earning $50,000 or less claimed the SALT deduction in 2017 as compared to over 90% of taxpayers earning $200,000 or more.

Federal expenditures designed specifically to assist renters also fall short, as middle- and even low-income people in need of housing assistance do not meet program qualifications. The Department of Housing and Urban Development (HUD) uses Area Median Income (AMI) as a reference point to categorize households by income tier and determine who qualifies for housing assistance. A household’s income relative to the median income in the area is represented as a percentage (e.g. 100% of AMI would apply to someone earning the equivalent of the median income in their area) and is used to place them somewhere on the scale. A household earning:

- <30% of the AMI is considered to be extremely low income

- <50% of the AMI is considered to be very low income

- <80% of the AMI is considered to be low income

- <120% of the AMI is considered to be moderate income

- <160% of the AMI is considered to be middle income

None of the major federal housing assistance programs serve households earning above 80% of the AMI, leaving moderate and middle-income families to fend for themselves. 80% of the AMI is the maximum income a household can earn and still be eligible for public housing or subsidized rent in a project-based rental assistance unit.

Some programs even exclude a large contingent of low-income households. For example, HUD offers a Low Income Housing Tax Credit (LIHTC) incentive for developers to construct new affordable housing units. To live in one of these units, a household must earn no more than 60% of the AMI. HUD also imposes a 60% AMI limit on beneficiaries of its HOME Investment Partnerships Program, which provides grants for states and municipalities to fund a range of activities related to providing affordable housing.

Housing Choice Voucher (HCV) programs, which subsidize the portion of rent that exceeds 30% of a household’s income for a moderately-priced unit, are especially efficient in allocating taxpayer dollars. According to Stephen Malpezzi of the Department of Real Estate at the Wisconsin School of Business, “for every taxpayer dollar spent on project-based/supply-side programs, households receive a benefit that they value at somewhere between 40 and 60 cents. For every taxpayer dollar spent on demand-side/voucher programs, households receive a benefit that they value somewhere between 80 and 90 cents.”

According to the left-leaning Center for Budget and Policy Priorities, the HCV program reduces poverty and housing instability, improves the mental and physical health of participants, and improves life outcomes for participants’ children. But the eligibility cutoff for the HCV program is especially low. Any household falling just above the threshold of “very low income”—or 50% of the AMI—is considered ineligible to receive a voucher.

Aside from the fact that these programs exclude many cost-burdened households, they are sometimes inaccessible even for families who do meet income qualifications. Due to HUD budget constraints, only about 25% of families eligible for Housing Choice Vouchers (HCV) actually receive them. And nobody receives a voucher immediately—eligible applicants must typically spend time on a long waiting list first. According to a 2015 report from the Congressional Budget Office, it would cost about $41 billion per year over a ten-year period to provide a voucher to every eligible household and eliminate the waiting list. Combined, the appropriations bill for FY2020 and the CARES Act allocate a total of just $25.15 billion to the HCV program.

To further complicate the process of renting or buying with a voucher, the HCV program is voluntary, and despite the fact that vouchers are reliable forms of payment, not all landlords are willing to accept them. While some denials may be the result of stereotypes about the program and its participants, landlords might also choose to deny voucher-holders due to the regulatory requirements that come with program participation. Participating landlords must complete extensive paperwork and comply with regular safety inspections of their rental properties.

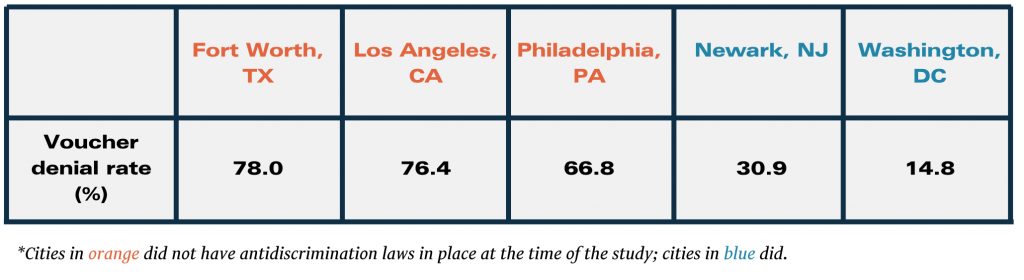

As of August 2020, 17 states, the District of Columbia, and several municipalities have enacted laws that protect voucher-holders from discrimination. But these laws cover less than half of all voucher households. In 2018, HUD conducted a study of landlords’ voucher acceptance rates across five U.S. cities: Fort Worth, Los Angeles, Newark, Philadelphia, and Washington, D.C. Results varied by city, but demonstrated that voucher denials were prevalent—especially in places without source-of-income antidiscrimination laws.

Some “solutions” make the problem worse

- Rent control policy is counterproductive

In response to shortages of affordable housing, some local governments (and some state governments) across the country have implemented rent control policies to place a cap on how much a landlord may charge for rent. However, mandatory rent controls often fail to achieve their intended outcomes and can even contribute to the problems they intend to solve. While a majority of U.S. states have recognized the damage these laws cause and have enacted laws to preempt or prohibit them, rent control policies continue to wreak havoc in several major cities experiencing housing shortages across the U.S.

These policies are beneficial to individual occupants in the short term but counterproductive in the long term because they distort the market in a way that exacerbates rising costs and inadequate supply. By placing a cap on developers’ potential earnings, rent control policy disincentivizes the construction of new housing in cities where supply is already scarce. Rather than conforming to rent control requirements, a developer can easily choose to build in another location where the policy is not in effect.

Developers who do build in rent-controlled jurisdictions often earn insufficient income from rent payments, leading them to cut corners on building maintenance. Rather than ameliorating the affordable housing shortage, rent control leaves cities with fewer, lower-quality affordable units. The policy does benefit those lucky enough to secure a rent-controlled unit, but it causes unjustifiable harm to a housing market in the long run.

“Next to bombing, rent control seems in many cases to be the most efficient technique so far known for destroying cities.” –Swedish economist Assar Lindbeck

A 1994 ballot initiative in San Francisco provides a natural case study of the effects of rent control. The initiative expanded the city’s rent control policy to apply to small, multifamily apartment buildings built before 1980. Stanford economists analyzed data from before and after the policy change and found that while tenants in rent-controlled units enjoyed lower rents as a result of the expansion, landlords whose properties were impacted by the expansion reduced the supply of rental housing (by converting them to condo units, for example) by about 15%. Similarly, a study conducted by MIT economists found that, after Cambridge, Massachusetts repealed its rent control policy in 1994, the number of permits issued for improvements on existing units and new construction increased by 20%.

- Inclusionary zoning: Best approached with caution

Not to be confused with upzoning, inclusionary zoning (IZ) is a type of policy that aims to produce affordable housing by incentivizing or mandating the inclusion of some number of below-market-price units in new multifamily construction. Lawmakers have implemented variations of this policy in over 900 jurisdictions in the U.S. in an effort to increase the availability of affordable housing and allow lower-income families to access the same amenities that draw wealthier people to the area. But a policy’s success or failure largely depends on the details of its design. Because this type of policy limits the profits of developers, the successful programs are the ones that offer incentives valuable enough to offset these costs. In strictly regulated markets, incentives like reduced parking requirements and density bonuses can counteract foregone profits and attract new development.

However, if not crafted carefully, IZ policies can produce outcomes similar to those produced by rent control. In 2017, Portland, Oregon enacted an inclusionary zoning requirement applicable to all new residential construction with 20 or more units. The city offered some incentives, but they were not valuable enough to be worthwhile for developers. Rather than taking on 20-plus-unit development projects and complying with IZ regulations, developers simply shifted their focus to smaller residential buildings. Two years after the law took effect, Portland saw a surge in permit applications for smaller multifamily structures and a 64% decline in those for 20-plus-unit buildings.

- Rent payment and eviction moratoriums can have short-term benefits but long-term downsides

The CARES Act included a provision that halted evictions for renters living in properties financed by federally backed mortgages. Several states have also passed their own eviction moratoriums. While these provisions have assisted some renters who have been unable to keep up with their monthly rent payments in the short term, they simply passed the financial responsibility from renters to their landlords. About half of all rental units nationwide are owned by large development firms, but the other half are owned by “mom-and-pop” landlords who rely on rental income for their own living expenses. The federal eviction moratorium ended on July 25, and tenants who were previously covered are now responsible for paying back all missed rent—even if their financial situation has not changed.

Solutions

For local governments:

No single solution can solve the affordable housing crisis overnight. But the enactment of policies that increase housing supply and the repeal of those proven to do the opposite are crucial first steps. No two housing markets are exactly alike, so localities must evaluate the consequences of each option and determine the specifics carefully. But cities and states looking for promising ways to expand housing supply can look to several localities that have recently passed reforms:

Upzoning: In 2019, Minneapolis became the first major city in the U.S. to abolish single-family zoning. Prior to the change, the construction of anything other than a detached single-family home was prohibited on about 70% of all residential land in the city. In addition to single-family homes, duplexes and triplexes are now permitted on this land. These types of sweeping proposals had failed in other cities, so to avoid a similar fate, the city solicited input from the community before releasing the final proposal. A comprehensive community engagement strategy and a compromise with the opposition (the original proposal sought to include fourplexes as well) were instrumental in the passage of the bill.

Repeal of parking minimums: In late 2018, San Francisco eliminated minimum parking requirements from its municipal code, becoming the largest American city to do so. In the decades leading up to the reform, San Francisco had taken a gradual approach to relaxing parking requirements to accommodate population growth. When the city’s Board of Supervisors released the proposal, it was framed as a small expansion of regulations already on the books that would alleviate the housing shortage, reduce traffic, and encourage sustainable modes of transportation. Legislators also emphasized that the elimination of parking minimums was not synonymous with a ban on parking—developers who wished to build parking would still be free, just not required, to do so.

Relaxation of density limits: In 2016, Fairfax County, Virginia increased the maximum allowed floor area ratio—a comparison of a building’s total floor area and the size of the lot it sits on—in areas surrounding Metro transit stations and commercial areas. The county’s Board of Supervisors chose this strategy to allow for increased population density without creating much additional car traffic.

For the federal government:

The federal government has a longstanding role in providing housing assistance to those unable to afford it. HUD subsidies and rental assistance programs are effective for those lucky enough to access them, but insufficient funding for these programs prevents millions of deserving people from reaping the benefits. Cutting program funds will only make this problem worse. And while state and local governments determine the specifics of land use policy, the federal government could use a lever to incentivize effective reforms.

Make zoning/land use reform a prerequisite to transportation funding

Some federal lawmakers have discussed an incentive program that would provide additional federal housing assistance funds to municipalities that enact zoning and land use reforms. But housing assistance may not be a good incentive for the cities that could benefit the most from enacting reforms. Wealthy communities typically have the most restrictive zoning regulations, and these places do not typically receive federal housing funding. Instead, transportation funding—which is more evenly distributed throughout all communities—could be a powerful incentive. Municipalities could be required to demonstrate the following to become eligible for federal surface transportation funding:

- A higher percentage of residential land zoned for multifamily housing and reasonable density limits (federal and state governments could establish minimum standards)

- An absence of rent control policy

- A repeal of any existing minimum parking requirements

While supply-side solutions should be the priority, two demand-side solutions—one for the short term and one for the longer term—have received bipartisan support:

Provide COVID-19 relief for landlords and lenders

Before the COVID-19 outbreak, in December 2019, Senators Michael Bennet (D-CO) and Rob Portman (R-OH) introduced the bipartisan Eviction Crisis Act. Using the broader framework of the original bill to address the specific crisis at hand, Bennet recently advocated in an op-ed for the allocation of $100 billion to local governments and nonprofits, who would then distribute this funding to landlords to cover unpaid rent. Patching up the disruption of unpaid rent would create a positive ripple effect across the economy. Direct assistance to landlords would reduce the burden on renters, and allow for both landlords and renters to catch up on payments to the businesses that provide them with essential services.

Enact legislation to combat source-of-income discrimination

During the 115th Congress, Senators Tim Kaine (D-VA) and Orrin Hatch (R-UT) introduced the Fair Housing Improvement Act of 2018, which would have prohibited landlords from discriminating against recipients of Housing Choice Vouchers or other alternative sources of income. The bill expired at the end of the legislative session without a vote on the floor. This type of policy has proven its effectiveness at the state level, and this federal legislation would assist all 2.2 million current voucher holders in their search for a place to live. Aside from widespread voucher discrimination, the HCV funding shortage also serves to limit the program’s reach. In the future, additional funding for HCV will be necessary to allow more eligible households to participate in the program and reap its benefits.