America’s 5G Moment of Truth

The future of technological and economic innovation will be redefined by 5G. Cutting-edge technologies—from self-driving cars to robotic surgery—will rely on widely available 5G for consistent, high-capacity, top-speed connectivity. According to a Global System for Mobile Communications (GSMA) Intelligence Report, 5G is expected to add $2.2 trillion to the global economy over the next 15 years, roughly 5.3% of total gross domestic product during this period.

The 1980s saw the emergence of the first American 1G network, which enabled the release of the Motorola DynaTAC, the first FCC-approved commercial portable cellular phone. The shoebox-sized cell phone needed to be charged for roughly ten hours and could be used for less than thirty minutes. After that, each new network generation yielded higher efficiency and reduced latency (delay time in data transference)—2G enabled texting, 3G enabled mobile web surfing, and 4G made applications like ride sharing and video streaming possible.

A 2019 5G Speedtest demonstrated a commercial download speed of 1.13 Gbps in Providence, RI—11 times faster than 4G. Eventually, 5G could clock in at 100 times faster. Once deployed, 5G could enable innovations like autonomous vehicles, virtual reality (VR), and Internet of Things (IoT) devices (objects like fridges, factory machines, and sensors that are connected to the internet). According to a February 2019 HarrisX poll, 72% of business decision makers agree that 5G benefits will be worth paying more for in their businesses, despite the fact that 5G is still not available in most places in the U.S.

Despite the growing importance of high-speed connectivity, the United States—which paced the world in developing and deploying so many other transformative technologies—is falling behind in the 5G race, while China sprints ahead. The leading American cellular companies—AT&T, T-Mobile Sprint, and Verizon—have only deployed commercial 5G networks within a tight radius of a handful of major cities, typically limited to customers with elite data plans. For now, the major difference between 4G LTE and 5G is just speed, but as coverage continues to roll out to new areas, more services that rely on instant connectivity should become possible.

In this paper, The New Center explains the potential applications of 5G-enabled services and devices, how America fell behind in the global race for 5G, and how we can get ahead.

How Does 5G Technology Work?

Data is transmitted along three “bands” of the radio spectrum, which are categorized as “low,” “mid,” and “high” bands. Each generation of cellular network technology has operated on a portion of that radio spectrum—1G relied on frequency bands between 850 MHz and 1.9 GHz, 2G and 3G primarily utilized the 850 MHz to 2.1 GHz band, and 4G utilized 600 MHz to 2.5 GHz.

Each spectrum band has different characteristics, making them ideal for different operations. Typically, low-frequency transmissions can cover long distances before losing their integrity, with the ability to penetrate dense objects like buildings, trees, and glass. However, significantly less data can be carried this way, making for lower speeds and increased latency. Conversely, higher-frequency transmissions can transmit massive amounts of data, but struggle to get through obstacles.

For the most effective 5G coverage, providers are utilizing all three bands:

- Low-band (sub-1GHz) spectrum—Spectrum is a finite resource, and low-band spectrum’s bandwidth is almost entirely depleted by LTE. T-Mobile secured a large portion of 600MHz spectrum at the 2017 Federal Communications Commission (FCC) auction in the hopes it would help the company facilitate a swift 5G rollout.

- Mid-band (1 GHz – 6 GHz) spectrum—It’s considered ideal for 5G because it can carry plenty of data while also traveling significant distances. Sprint has the majority of unused U.S. mid-band spectrum.

- High-band (24Ghz – 40Ghz) or millimeter wave (mmWave) spectrum—This band could provide speeds up to 10Gbps with minimal latency. However, high-band requires significantly more infrastructure because it only extends around 200 meters and has difficulty penetrating through objects. Providers would need to posit thousands of “small cells” (low-powered cellular radio access nodes with short ranges) and other technologies to offer comprehensive 5G service. Verizon dominates the U.S. millimeter wave spectrum, having secured 4,940 licenses through March 2020’s Auction 103 and the acquisition of several communications companies, with AT&T coming in second.

How Do FCC Spectrum Auctions Work?

In the U.S., any entity or individual who wants to broadcast using radio waves must secure a license from the Federal Communications Commission (FCC). The FCC hosts frequent “auctions” to allocate portions of the electromagnetic spectrum for mobile communications to companies which are (a) found “eligible,” or capable of actually utilizing the spectrum as intended, and (b) can afford to pay the hefty bill upfront, with recent 5G auctions raking in billions of dollars in total proceeds.

What is the Potential Economic Impact of 5G?

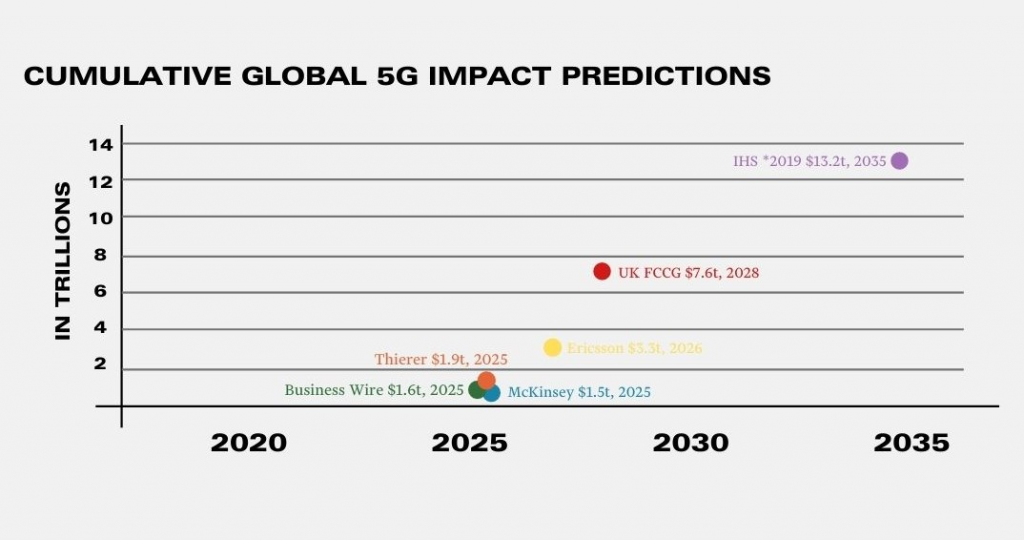

Several economic forecasting groups, communications firms, and consulting companies have offered predictions for the economic impact of 5G over the next ten years. While the exact numbers vary between different models, 5G could add more than $1 trillion in global economic output by 2025 according to most estimates.

One of the most extensive studies into 5G’s potential economic impact was commissioned by Qualcomm Technologies in 2019, and carried out by the independent consultancies IHS Markit, Penn Schoen Berland, and the Berkeley Research Group. They approximated that the global 5G value chain will generate $3.6 trillion in economic output and 22.3 million jobs by 2035. This would make the 5G value chain larger than today’s entire mobile value chain, or the revenue that mobile technology facilitates across all sectors.

“5G will be a new kind of network, supporting a vast diversity of devices with unprecedented scale, speed and complexity. 5G will have an impact similar to the introduction of electricity or the car, affecting entire economies and benefiting entire societies.”—Steve Mollenkopf, CEO of Qualcomm

According to an April 2019 HarrisX poll, business decision makers expect the industries most impacted by 5G will be telecommunications, health and emergency services, transportation, and engineering and manufacturing. This list is by no means exhaustive, but illustrates how some major sectors are expected to utilize 5G in their daily functions:

Manufacturing

5G technology is already being rolled out in smart factories to make floor production more accurate, efficient, and cost-effective. For example, augmented reality glasses are being used by production engineers to overlay images onto broken components. These glasses overlay images of cables, bolts, part numbers, and assembly instructions to ease the time-consuming process of trying to locate the problem.

Transportation

5G could enable near-instantaneous sharing of data on the road to give cars the ability to essentially “talk” to each other in real time, and sense other objects and people in their surroundings. This could improve the flow of traffic and prevent more of the 94% of car crashes caused by human error. 5G could also enable more efficient freight transport, where data sharing can be used to streamline shipping, track goods, prevent cargo theft, and reduce fuel inefficiencies and pollution.

Media

5G could enable a seamless viewing experience in streaming live TV, movies, music, and video games. Download speeds could increase more than tenfold over 4G, meaning HD movies could be downloaded in just a few seconds.

Health

Health providers are continually gathering massive amounts of medical data such as multi-gigabyte x-ray images, nonstop-monitoring wearable medical devices, and AI-powered diagnostic programs. 5G will enable providers to capture, review, and share large files without slowing down their existing wired networks.

One of the most impressive potential use cases is “remote surgery” conducted over 5G. In 2019, a doctor located in the southern Chinese city of Sanya used 5G-enabled robotic surgical instruments to implant a stimulation device in the brain of a Parkinson’s patient in Beijing, nearly 2,000 miles away. This procedure would have been impossible using 4G, which can cause lag times as much as two seconds, far too long for an intensive and exacting neurosurgery.

Shifting Generational Leadership in Mobile Technology

Where It All Began

In 1979, Nippon Telegraph and Telephone (NTT) launched the first generation (1G) of mobile networks in Tokyo. Within five years, NTT provided the entirety of Japan with 1G accessibility. Through 1981 and 1982, 1G was launched in Denmark, Finland, Norway, and Sweden using the Nordic Mobile Telephone standard—a protocol that would later be replicated by Saudi Arabia, Russia, the Baltics, and multiple other Asian countries. In 1983, the U.S. approved the first 1G commercial operations, which were launched by the then-so-called Ameritech using Motorola’s DynaTAC mobile phone. Several other countries like Canada, the U.K., Malaysia, Mexico, and China would unveil their first networks in the 1980s.

As to be expected from the first iteration of any technology, 1G suffered from a litany of setbacks. The sound quality of calls was poor—if one could manage to place the call in the first place because of the spotty coverage. Calls were unencrypted, enabling anyone with a radio scanner to eavesdrop. Different operators didn’t support “roaming,” or the ability to connect to the network of a different carrier in a different geographic region. Additionally, the technology was so incredibly expensive (DynaTAC cost $3,995 price tag, or $9,660 in today’s money) that most Americans didn’t use cell phones until 2G had already arrived.

Europe Coordinates Efficient 2G Rollout

Beginning in the 1980s, the European Commission signed a joint development agreement to allocate spectrum for the Global System for Mobile Communications (GSM), standards for 2G digital cellular networks. By 1994, early European adopters had reached more than 70% 2G wireless penetration (the percentage of unique 2G mobile users compared the population), while the US only had 0.1% penetration. The U.S. wouldn’t catch up to Europe with 2G until 2003, when Japan and parts of Western Europe were already rolling out their 3G networks.

European 2G dominance enabled the rise of the European telecommunications giants including Ericsson (Sweden), Nokia (Finland), and Siemens (Germany), which still control a significant share of the wireless equipment market. In 1993, Ericsson made up 60% of the global digital cellular equipment market, while in 2019 the company still accounted for 43% of the mobile system’s global market share. According to a report by Recon Analytics, early 2G leadership “yielded tangible economic benefits for European countries, including the strong economic contributions of wireless manufacturers to their balance of trade, the employment of hundreds of thousands, and the generation of intellectual capital and property rights.”

The Global System for Mobile Communications allowed European companies to coordinate spectrum allocation and roll out their wireless networks. GSM was created by the European Telecommunications Standards Institute, an industry consortium that licensed various companies to create mobile technology affordably. Conversely, the U.S. government allowed mobile carriers to pursue multiple different network standards, including GSM and a less common method called “code-division multiple access” (CDMA). CDMA is largely owned by the U.S. company Qualcomm, which partnered with Verizon to create cell sites that could handle more network capacity than GSM.

However, having multiple standards meant that carriers’ plans weren’t mutually compatible—consumers couldn’t keep their phones when switching from Verizon, which operated on CDMA, to T-Mobile, which used GSM. Additionally, operating on CDMA made service less accessible and affordable because it was built by Qualcomm using their patented technology, which the company didn’t license to competitors like Ericsson until years later. According to Recon Analytics’ retrospective analysis, while the American approach may have afforded greater technological experimentation, “a fragmented market based on competing standards made it more challenging for U.S. wireless equipment sellers to amass a large customer base.”

Japan Launches 3G With Mobile Application Innovation

In late 2001, Japan’s largest mobile phone operator NTT DoCoMo launched its third generation network that would accommodate high bandwidth applications. It was called “Freedom of Mobile Multimedia Access (FOMA),” which was faster and higher powered than the European-pioneered 2G network. Most notably, FOMA supported videophone and “i-motion,” which allowed subscribers to obtain video content at speeds of up to 384kbps, nearly four times the download speed possible on a 2G network.

At the same time, European mobile operators were being hampered by EU regulation that prohibited them from repurposing their existing 2G spectrum for 3G. Instead, they had to wait for a specific 3G auction and win bids to deploy 3G services. This drove astronomical auction prices and slowed down allocation for spectrum licenses, translating into higher prices for consumers.

For example, in the U.K., thirteen companies competed to win an auction for just five 3G spectrum licenses in 1999. This one auction alone raked in £22.5 billion for the U.K. government, which is more than the U.S. secured in auctions for the six years prior, despite the U.S. being over four times the size of the U.K. But it came at the cost of forcing British telecoms—who were prohibited from sharing the licenses among one another—to acquire enormous debts and resulting drops in share prices, making it difficult for them to fund 3G infrastructure rollout.

The U.S. Leads the 4G Ecosphere

Following Japan’s i-mode success, the U.S. began to ramp up their 3G penetration in the wake of the introduction of high-powered smartphones. From the release of the iPhone 1 in 2007 to 2011, the U.S. added around 20 percentage points a year to its 3G penetration rate.

This swift transition was made possible by the FCC’s sale of more than 3,000 mid-band spectrum licenses between 2005 and 2008. Additionally, in 2009, the FCC enacted a 90-day shot clock to require local governments to approve or reject telecommunication infrastructure applications. If the local government did not process an operator’s request in that time, the application was automatically approved.

While much of Western Europe was still hindered by requirements to issue new 4G-specific licenses, Japan and the U.S. started quickly building their networks and applications in 2011. The U.S. allowed telecom operators to use their spectrum allocations flexibly for new technologies while quickly auctioning off highly desired frequencies. Newfound spectrum availability and accelerated tower siting rules fueled U.S. 4G-enabled innovation, including cutting-edge iPhones and applications like ridesharing, high-definition video conferencing, and augmented reality.

At the start of 2011 in Japan, domestic firms made up over 75% of all mobile shipments and Apple was the only foreign firm to make the top five in terms of market share. By 2014, Apple had become the top firm in terms of market share, with other non-Japanese firms coming in close behind. Despite Japan pioneering the global rollout of 3G, the U.S. was able to set pace for the world in 4G-enabled wireless innovation and value creation.

China Outpaces the U.S. in 5G Rollout

In 2009, Swedish mobile network operator Teliasonera set out to build one of the five earliest national 4G networks and contracted the Shenzhen-based company Huawei, which at the time only represented 1.2% of the mobile phone market. Soon after, Huawei would secure a large contract to completely replace Norway’s network infrastructure, a deal worth a reported €170m over six years that displaced former Nordic-owned suppliers like Ericsson and Nokia. The Chinese newcomer would complete the network swap faster and cheaper than expected—Norway achieved the third-highest 4G LTE penetration of any country by 2017.

Founded in 1987 by Ren Zhengfei, a former engineer for the People’s Liberation Army, the Huawei name was a portmanteau of Zhonghua youwei (“China has promise”). Despite beginning with only a personal investment of $5,000 from Ren and a limited Asia-specific customer base, Huawei began exporting globally within two decades, eventually expanding beyond network equipment into data storage, consumer smartphones, laptops, wearables, and software. Today, Huawei accounts for 28% of the telecom equipment market, compared to just 16% for Nokia and 14% for Ericsson.

Now, Huawei is a leading supplier of the infrastructure for the global 5G rollout. Though the extent of China’s domestic 5G network is opaque, Chinese telecom companies claim to have the largest 5G consumer network in the world. Jefferies Group analysts predict that China will have 110 million 5G users, or around seven percent of the country’s population, by the end of this year.

However, as Chinese telecom companies like Huawei and ZTE have expanded, they have been embroiled in political scandal, facing accusations by governments and their commercial rivals of intellectual property theft, aiding human rights abuses, subverting international sanctions, and facilitating government espionage. Most notably, Huawei critics have pointed to its estimated $75 billion in ties to the Chinese government—$48 billion in support from state lenders from loans, credit lines and other support, along with $25 billion in tax incentives.

One major cybersecurity concern of the U.S. government is the Chinese National Intelligence Law, which allows Beijing to inspect all data collected by Huawei or any other domestic firm. Article 7 of the law states that “any organization or citizen shall support, assist and cooperate with the state intelligence work in accordance with the law.” This effectively permits the Chinese government to put “backdoors” into company hardware and software, enabling 5G networks to be used for government espionage. Huawei has stated that it would never turn over Americans’ data to the Chinese government, even if required by law.

However, legal experts have argued that Huawei and other companies wouldn’t have a choice. Jerome Cohen, a New York University law professor and Council on Foreign Relations adjunct senior fellow, told CNBC, “there is no way Huawei can resist any order from the [People’s Republic of China] Government or the Chinese Communist Party to do its bidding in any context, commercial or otherwise. Huawei would have to turn over all requested data and perform whatever other surveillance activities are required.”

For the past several years, the U.S. and its allies have spearheaded efforts to blacklist Huawei in 5G supply chains and require companies to have special licenses to ship products to the company. While Huawei argues these moves are purely to undercut Chinese competitiveness, multiple governments, industry groups, and intelligence agencies argue that there is ample reason for concern.

What Has Slowed U.S. Rollout?

Much of U.S. Mid-Band Spectrum is Reserved for the Military

In China, 5G has largely been rolled out using mid-band spectrum, the so-called “Goldilocks of spectrum,” because of its wide transmission distances and fast speeds. Conversely, the U.S. has primarily allocated the other two bands: (a) super-fast, highly localized high-band spectrum that requires multiple small cells, and (b) slower-speed, but expansive, low-band spectrum. As a consequence, 5G in China requires significantly less network infrastructure—a single cellular tower in China can cover the same radius as 100 high-speed American towers.

Sprint is the only commercial network operator with rights to a significant chunk of U.S. mid-band spectrum. Since the 1960s, most mid-band frequencies have been divided among various government agencies, with the bulk going to the U.S. Department of Defense, which uses the airwaves for military communications and research. However, many of the frequencies are going unused, driving up the cost of spectrum and blocking 5G rollout.

In April 2019, the Defense Innovation Board, a Pentagon advisory board of Silicon Valley executives, suggested that the military release some mid-band frequencies to telecom operators. Brendan Carr, one of five FCC commissioners, stated that the FCC and Pentagon were in talks to push this proposal forward, though U.S. wireless carriers have yet to receive any licenses.

Spectrum & Infrastructure Are More Costly in the U.S.

According to a report from GSMA Intelligence, U.S. wireless operators are expected to outspend their Chinese counterparts on 5G capital expenses by 58%, $284 billion to $179.8 billion, over the next five years. This is largely because there are some necessary expenses to setting up 5G which are much cheaper in China’s operating environment.

If a mobile operator wants to offer 5G, it needs to (a) secure spectrum, (b) find unused plots of land to set up cellular towers, and (c) build the tower and install supplementary hardware. However, a mobile operator doesn’t build this infrastructure from scratch, but instead contracts real estate and telecommunications equipment companies that lease their cellular sites.

In the U.S., wireless carriers spend billions in spectrum auctions, acquiring real estate, building cellular towers, and securing supplementary hardware. Conversely, the Chinese government offers carriers discounted spectrum and real estate rates, as the government controls land-use rights. China Tower, the state-owned telecommunications real estate firm, builds cellular towers for all three Chinese wireless carriers, primarily on top of state-owned land. As a result, the country is on pace to have at least 150,000 wide-area base stations necessary for 5G rollout available for public use by the end of the year, while the U.S. will only have 10,000.

In America, the vast majority of the land and rooftops ideal for communications towers are privately owned. The average rent for a ground lease is around $1,300 a month, while a typical steel cellular tower costs $80,000. The process of finding available land and constructing a single tower typically takes between one and six months—to meet 5G mobile demand, the U.S. needs to construct hundreds of thousands of these towers.

China’s government regulator mandates its carriers to share towers, cutting the cost of equipment and energy by sharing power converters, fiber-optic cables, and other equipment on or around the towers. Most U.S. towers have more than one tenant, but there’s an average of 1.5 tenants per tower—half of China’s average of three. Additionally, U.S. carriers are reluctant to share fiber-optic cable with their competitors, meaning each operator must invest heavily in digging new lines for wires.

Lack of Domestic Telecom Equipment

In addition to the cost of basic infrastructure, operators must purchase telecom equipment like radio access networks, which is not widely available from U.S. manufacturers. Huawei hardware is highly advanced and cheaper than its European counterparts—by 20% or more. Since U.S. companies are prevented from using Huawei products due to security concerns, however, they must buy more expensive European products.

New Center Solutions

In late 2019, a bipartisan group of senators from the committees on Foreign Relations, Homeland Security, Intelligence, and Armed Services expressed concern with a lack of a “coherent national strategy” on 5G. In a letter to the White House, the senators lamented:

“5G represents the first evolutionary step for which an authoritarian nation leads the marketplace for telecommunications solutions… We cannot rely exclusively on defensive measures to solve or mitigate the issue, but rather we must shape the future of advanced telecommunications technology by supporting domestic innovation through meaningful investments, leveraging existing areas of U.S. strength, and bringing together like-minded allies and private sector expertise through a sustained effort over the course of decades, not months.”

What has worked for China won’t necessarily work for the U.S. In a country built on principles of property rights and free enterprise, the U.S.’s path to 5G success looks radically different. We can, and should, be doing more to encourage U.S. telecommunications sector research and development through a coordinated government approach, clear standards, and efficient regulatory operations.

Promoting Inter-Agency Coordination

Cooperation is challenging when multiple agencies have overlapping jurisdictions over a given finite resource, and spectrum is no exception. For example, the FCC faced pushback from the National Oceanic and Atmospheric Administration (NOAA) when conducting its Spectrum Frontiers auction—the NOAA chief warned members of Congress 5G deployments using 24 GHz spectrum could reduce the accuracy of weather forecasting by 30%. Similarly, after the FCC granted applications to roll out a low-power nationwide broadband network, the Department of Defense and 12 other federal agencies publicly opposed the proposal, arguing that the move could cripple GPS networks.

Without a national strategy, each telecommunications-adjacent agency will continue to execute its own singularly-focused mandate, rather than identifying national goals and potential barriers that do not cleanly fall into a single division. It may take a president and Congress uniting to break down the parochial government agency interests that to date have stymied broader 5G adoption in the U.S.

The White House and Congress need to do a much better job of coordinating with agencies to tackle the largest obstacles to fifth generation technologies, such as allocating spectrum efficiently, promoting innovation, and securing equipment and infrastructure supply chains.

Expanding R&D Opportunities

The federal government can take the lead to help identify opportunities to extend and deepen federal support for R&D and cooperative efforts to drive research into production. One such opportunity to support next-generation innovation may be the bipartisan, bicameral Endless Frontier Act. This act would expand the National Science Foundation (NSF)—to be renamed the National Science and Technology Foundation (NTSF)—and provide the group $100 billion over five years to advance technology in 10 critical focus areas, including “advanced communications technology” like 5G and 6G. To read more about the Endless Frontier Act, see The New Center’s forthcoming issue brief analyzing the bill’s potential impact on American innovation and competitiveness.